Tired of Feeling Lost in the Home Loan Maze?

Get 5 Insider Secrets from NAR(National Association of Realtors) that Make Navigating Your Loan Simple and Stress-Free!

I consent to receive calls and texts from DreamX Homes & Glasshouse Realty Group for real estate information and assistance. You can unsubscribe anytime.

The Ultimate Guide to Monthly Payment Calculations

The Ultimate Guide to Monthly Payment Calculations

A monthly payment calculator is an essential tool for anyone planning to buy a home, car, or make other sizable purchases. It helps you understand the financial commitment you're about to make. Using it, you can quickly assess:

- What you can afford monthly based on your budget.

- Different loan terms, like 10-, 15-, or 30-year mortgages and how they affect your payments.

- The impact of interest rates on your total monthly cost.

By plugging in details like the loan amount, interest rate, and repayment period, this calculator shows you a clear breakdown of your expected monthly expenses.

Homeownership is often seen as the fulfillment of a dream, but careful budgeting is key. As Mark Hamrick of Bankrate says, "Being conservative and cautious with a home purchase is advisable." This sentiment rings true, especially when juggling additional financial goals like saving for emergencies or retirement. Using a monthly payment calculator provides transparency and aids in informed decision-making.

Understanding Monthly Payment Calculations

When it comes to understanding monthly payment calculations, several key elements are at play. These include loan types, interest rates, the principal amount, and the loan term. Each of these factors can significantly impact your monthly payments.

Loan Types

Different loans serve different needs. Common loan types include:

-

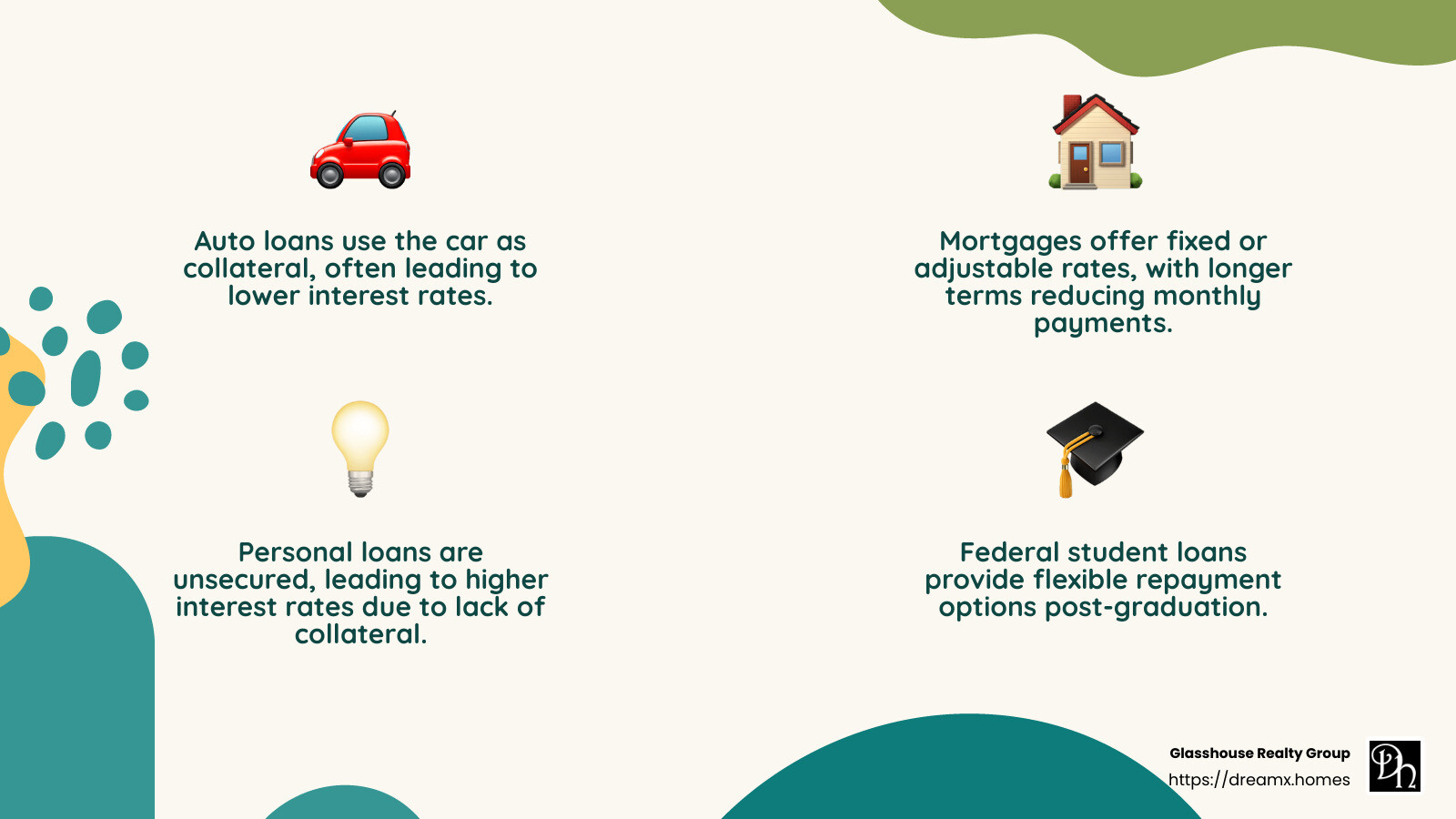

Auto Loans: These are typically secured loans, meaning the car itself serves as collateral. They often have shorter terms, like 3 to 7 years, and competitive interest rates.

-

Mortgages: These are long-term loans, usually 15 to 30 years, used to purchase a home. Mortgages can be fixed-rate, where the interest rate remains the same, or adjustable-rate, where it can change over time.

- Personal Loans: These are usually unsecured, meaning they don't require collateral. They have terms ranging from 2 to 5 years and can be used for various purposes.

- Student Loans: These are designed for educational expenses. Federal student loans often have more favorable terms than private ones.

Interest Rates

Interest rates are the cost of borrowing money. They can be fixed or variable:

- Fixed Rates: Stay the same throughout the loan term. This means your monthly payment remains constant, making budgeting easier.

- Variable Rates: Can change over time, which might lead to fluctuating monthly payments.

Interest rates are influenced by factors like your credit score, loan type, and market conditions. Generally, loans with longer terms have higher interest rates.

Principal

The principal is the amount you borrow. Over time, as you make payments, the principal decreases. In the early stages of your loan, a larger portion of your payment goes toward interest. As the loan matures, more goes toward reducing the principal.

Loan Term

The loan term is the duration over which you agree to repay the loan. Shorter terms typically mean higher monthly payments but less total interest paid. Conversely, longer terms lower your monthly payment but increase the total interest.

Understanding these components helps you make informed financial decisions. By using a monthly payment calculator, you can see how adjusting each element affects your payment. This is crucial for effective budgeting and financial planning.

How to Use a Monthly Payment Calculator

A monthly payment calculator is a powerful tool to help you understand and manage your finances. With it, you can estimate your monthly loan payments and see how changes in variables like interest rates and loan terms affect your budget.

Input Values

To get started, you need to input a few key details into the calculator:

-

Loan Amount: This is the principal amount you plan to borrow. Enter the total amount of the loan you need.

-

Interest Rate: Input the annual interest rate for the loan. If you have a fixed-rate loan, this number will remain the same. For variable-rate loans, this can fluctuate.

- Loan Term: Enter the duration of the loan in years. Common terms are 15, 20, or 30 years for mortgages and 3 to 7 years for auto loans.

- Down Payment: If applicable, include the amount you plan to pay upfront. This reduces the total loan amount and can lower your monthly payments.

- Additional Costs: Some calculators allow you to include property taxes, homeowners insurance, or HOA fees. These are important for getting a complete picture of your monthly obligations.

Amortization

Amortization refers to the process of spreading out a loan into a series of fixed payments over time. When you use the calculator, it will show you an amortization schedule, which breaks down each payment into principal and interest components.

- In the early years, a larger portion of your payment goes toward interest.

- Over time, more of your payment will go toward reducing the principal.

This schedule is crucial for understanding how your loan balance decreases over time and can help in planning for additional or early payments.

Budgeting

Using a monthly payment calculator is a vital step in budgeting. Here's how it helps:

-

Estimate Affordability: By adjusting the loan amount or term, you can see what fits comfortably within your monthly budget.

-

Plan for Future Expenses: Knowing your monthly payment helps you plan for other financial goals, like saving for retirement or a vacation.

- Compare Loan Options: Quickly compare different loan scenarios to find the best fit for your financial situation.

By understanding the inputs and outputs of a monthly payment calculator, you can make informed decisions that align with your financial goals. This tool is not just for estimating payments but also for crafting a robust financial plan.

Types of Loans and Their Impact on Monthly Payments

When it comes to loans, different types can have various impacts on your monthly payments. Understanding these differences can help you make better financial decisions.

Auto Loans

Auto loans are designed to help finance the purchase of a vehicle. These loans are typically secured, meaning the car itself acts as collateral. Because of this, interest rates on auto loans are often lower than unsecured loans. However, if you fail to make payments, you risk losing your vehicle.

- Term: Auto loans usually range from 3 to 7 years.

- Interest Rates: Rates can vary based on your credit score and whether the car is new or used.

- Impact: Longer terms may lower your monthly payments but increase the total interest paid over the life of the loan.

Mortgages

Mortgages are loans used to purchase real estate. They are typically the largest loans individuals take on and come with specific terms and conditions.

- Term: Common terms are 15, 20, or 30 years.

- Interest Rates: Fixed or adjustable rates are available, with fixed rates providing predictability in monthly payments.

- Impact: A longer term reduces the monthly payment but increases the total interest paid. Shorter terms have higher payments but lower total interest costs.

Personal Loans

Personal loans are versatile and can be used for various purposes, from home improvements to consolidating debt. These loans are usually unsecured, meaning they don't require collateral.

- Term: Typically ranges from 2 to 5 years.

- Interest Rates: Rates depend heavily on your credit score and the lender's terms.

- Impact: Because they are unsecured, personal loans often have higher interest rates than secured loans, affecting the monthly payment amount.

Student Loans

Student loans are specifically for educational expenses. They can be either federal or private, with federal loans generally offering better terms and protections.

- Term: Terms can vary, often extending up to 10 years or more.

- Interest Rates: Federal loans have fixed rates, while private loans may offer variable rates.

- Impact: Federal loans often have more flexible repayment options, which can help manage monthly payments post-graduation.

Each loan type has its unique features and implications for your monthly budget. By considering the term, interest rate, and loan type, you can better understand how each loan will impact your finances. Using a monthly payment calculator can further assist in visualizing these impacts and planning your budget accordingly.

Benefits of Using a Monthly Payment Calculator

Using a monthly payment calculator can be a game-changer for your financial health. Let's break down why this tool is so beneficial:

Financial Planning

A monthly payment calculator helps you see the big picture. By inputting different loan scenarios, you can understand how much you're committing to each month. This insight is critical for setting realistic financial goals. Whether you're planning to buy a house or a car, knowing your monthly payment helps you see if it fits within your overall budget.

Debt Management

Managing debt can be tricky, but a monthly payment calculator simplifies it. You can experiment with different loan terms and interest rates to find a monthly payment that works for you. This tool can also show how extra payments can reduce your debt faster. By understanding these dynamics, you can make smarter decisions that minimize your debt burden over time.

Savings

Who doesn't love saving money? With a monthly payment calculator, you can find ways to save on interest payments. For instance, it can help you decide whether a shorter loan term, which often comes with higher monthly payments, might save you money in the long run by reducing the total interest paid. It’s a great way to ensure you're not stretching your finances too thin while also maximizing long-term savings.

A monthly payment calculator provides clarity and control over your financial commitments. It empowers you to make informed choices, ensuring that your financial decisions align with your goals and lifestyle.

Frequently Asked Questions about Monthly Payment Calculations

How do you calculate a monthly payment?

Calculating a monthly payment involves understanding the relationship between the loan amount, interest rate, and loan term. The basic formula used is:

[ M = \frac{P[i(1+i)^n]}{(1+i)^n-1} ]

Where:

- M is the total monthly payment.

- P is the principal loan amount.

- i is the monthly interest rate (annual rate divided by 12).

- n is the number of payments (loan term in years multiplied by 12).

This formula helps to determine how much you need to pay each month to repay your loan over a specified period.

How much house can I afford for $800 a month?

To figure out how much house you can afford for $800 a month, consider the loan terms, interest rate, and any additional costs like taxes and insurance. Using a monthly payment calculator, you can input your desired monthly payment and see how it aligns with various home prices and down payment amounts.

For instance, if you have a 30-year mortgage with a 4% interest rate, a larger down payment will reduce the loan amount and potentially increase the house price you can afford. Affordability is influenced by these factors, so experimenting with different scenarios can give you a clearer picture of your budget.

What is the formula for calculating monthly mortgage payments?

The formula for calculating monthly mortgage payments is similar to the one used for general loans, but it often includes additional components like property taxes and insurance. The core formula remains:

[ M = \frac{P[i(1+i)^n]}{(1+i)^n-1} ]

In this context:

- P is the principal loan amount (after the down payment).

- i is the monthly interest rate.

- n is the total number of payments over the loan term.

By using a monthly payment calculator, you can easily input these values along with any extra costs, like homeowners insurance or HOA fees, to get a comprehensive view of your monthly obligations.

Understanding these calculations helps you make informed decisions about your mortgage options, ensuring they align with your financial capabilities and long-term goals.

Conclusion

At Glasshouse Realty Group, we believe that buying or selling a home should be a transparent and stress-free experience. That's why our team at DreamX.Homes is dedicated to providing you with personalized guides and insights custom to your unique needs.

Our services extend beyond simple transactions. We leverage advanced tools, including AI for home valuation, to ensure you have the most accurate information at your fingertips. Our focus on transparent transactions means you can trust us to guide you through every step of the home-buying or selling process.

Whether you're calculating your mortgage with our monthly payment calculator or exploring the vibrant real estate markets of Cincinnati, Dayton, and Springfield, we're here to help you make informed decisions.

Ready to take the next step in your home journey? Explore our mortgage calculator to see how much home you can afford and start planning your future today.

Categories

- All Blogs 92

- Boosting Home Value 3

- Buyer Resources 13

- Eco-Friendly Upgrades 1

- First-Time Buyer Tips 2

- Home Buying & Selling 3

- Home Improvement & Staging 5

- Investment & Financing 14

- Local Attractions & Schools 5

- Local Market Trends 8

- Local Policy Changes 2

- Market & Industry News 2

- Market Insights 6

- Mistakes to Avoid 1

- Mortgage & Financing 22

- Neighborhood Spotlights 12

- Neighborhoods & Lifestyle 18

- New Construction 10

- Real Estate News & Updates 4

- Real Estate Technology 2

- Seller Resources 4

- Staging Tips 2

- Sustainability 3

Recent Posts

Tired of Feeling Lost in the Home Loan Maze?

Get 5 Insider Secrets from NAR(National Association of Realtors) that Make Navigating Your Loan Simple and Stress-Free!

I consent to receive calls and texts from DreamX Homes & Glasshouse Realty Group for real estate information and assistance. You can unsubscribe anytime.

"My job is to find and attract mastery-based agents to the office, protect the culture, and make sure everyone is happy! "