Tired of Feeling Lost in the Home Loan Maze?

Get 5 Insider Secrets from NAR(National Association of Realtors) that Make Navigating Your Loan Simple and Stress-Free!

I consent to receive calls and texts from DreamX Homes & Glasshouse Realty Group for real estate information and assistance. You can unsubscribe anytime.

Buying A House With An FHA Loan In Ohio: Complete 2025 Guide

People often ask me which loan they should go for. I am sure that you already heard about a few types of loans. But before you go for one, give me an opportunity to tell you why you should go for an FHA loan Ohio. You can easily start by giving a 3.5% down payment on the home price you choose. You heard me right, buddy. FHA loan downpayment is low, which is good news for home buyers like you.

Let's assume the price of the home you have chosen is $2,25,000. That means you could buy a house with an FHA loan and put down as little as $7,875—just 3.5% of the home’s price. Pretty amazing, right? That’s the kind of number that makes owning a home feel totally doable.

FHA loans are particularly designed to make homeownership accessible, even if you’re not rolling in cash or have less-than-perfect credit.

In this guide, I’ll walk you through everything you need to know about FHA loans in Ohio—from requirements and benefits to challenges and tips for first-time buyers. Whether you’re eyeing a cozy home in Dayton or a charming property in Cincinnati, I’ve got you covered. I am going to take a coffee, you can take too, or tea if you prefer, and let's get started—you'll want to stay around for this one!

What is an FHA Loan? Let me explain to you.

Definition of an FHA Loan

An FHA loan is like a financial superhero! Yep, a superhero in this loan world. It swoops in when you need a little extra help to buy a home. FHA Loan Ohio is backed by the Federal Housing Administration. These loans give people like you and me a chance to buy a house without needing a huge down payment or a perfect credit score.

Let me give you an example. If you’re buying a $200,000 house with a conventional loan, you might need to put down 20% upfront; that’s a whopping $40,000. Ouch! But with an FHA loan, you only need 3.5%, or $7,000. Big difference, right?

Why You Should Choose an FHA Loan in Ohio?

Ohio’s housing market is always known for its affordability, and FHA loans are a perfect match. If you are looking for an affordable home in Dayton or historic properties in Cincinnati, trust me, these loans can make the process a whole lot easier.

Here is one of the best things you should know. They’re super flexible. Even if your credit score isn’t where you’d like it to be, you might still qualify. Plus, FHA loans often come with lower interest rates compared to other options, so you could save thousands over the life of your loan.

FHA Loan Requirements You Should Fulfil in Ohio

Minimum Credit Score You Should Have for an FHA Loan

Let’s talk about credit scores, which are one of the biggest concerns for many buyers, and you should get an idea of it. For an FHA loan in Ohio, you need a lowest credit score of 580 to qualify for a 3.5% down payment. But even if your score is between 500 and 579, don’t give up! You might still qualify if you can put down 10% instead.

Fun fact: The average credit score in Ohio is about 716, which is above the national average. But even if you’re not quite there, FHA loans are a fantastic option to explore.

Debt-to-Income Ratio Requirements

Your debt-to-income ratio (DTI) is a fancy term for how much of your income goes toward paying off debts each month. Most FHA lenders in Ohio want to see a DTI of 43% or less, but some may allow up to 50% if you’ve got other strengths, like a steady job or savings.

For example, if you earn $4,000 a month, your total monthly debt, including your estimated mortgage, shouldn’t exceed $1,720.

Down Payment Requirements

Here’s the best part: FHA loans only require a 3.5% down payment. So, for a home priced at Ohio’s median of $215,000, your down payment would be $7,525.

Steps You Should Take to Apply for an FHA Loan in Ohio

Prequalification and Financial Preparation

The first step to snagging an FHA loan is prequalification. Think of it as your financial dress rehearsal. It gives you a clear idea of what you can afford and lets sellers know you’re serious. You can go here for fast prequalification.

I would suggest that you start by checking your credit score; you can see a free report at AnnualCreditReport.com and fix any errors. Then, you can start budgeting for upfront costs like your down payment and closing costs. Did you know closing costs in Ohio usually run around 2–5% of the home’s price? Planning ahead of time may help you avoid a lot of difficulties.

Finding an FHA-Approved Lender

Not all lenders offer FHA loans, so you’ll need to find one that’s FHA-approved. The good news? Ohio has plenty of options, from big-name banks to local credit unions. Use HUD’s online tool to search for approved lenders in your area. You can reach Bill Hudson, who is an FHA-Approved Lender with 27 years of experience.

When choosing a lender, I would suggest that you should not just focus on interest rates. You should ask about fees, the customer service they provide, and how well they know Ohio’s housing market. A great lender will guide you through the process and answer all your questions (even the ones you think sound silly).

Submitting an FHA Loan Application

At this stage, if you have already found your lender. Now, it's time for you to apply. You should be prepared to provide these documents:

- Pay stubs or proof of income

- Tax returns from the past two years

- Bank statements

- Information on any outstanding debts

The underwriting process might feel a little overwhelming for you, but you should take it one step at a time. There is nothing to worry about. Your lender is there to help.

What Are FHA Loan Limits in Ohio for 2025?

Overview of Loan Limits

In Ohio, FHA loan limits vary depending on the county where you’re buying. For 2025, the FHA loan limit for a single-family home is $472,030 in most areas. However, in higher-cost areas, such as parts of Columbus and Cincinnati, the limit can go up to $600,000.

These limits are updated annually by the Federal Housing Administration to ensure they align with current housing market trends, so they give buyers enough flexibility to find a home that fits their needs.

How Loan Limits Impact Your Buying Options

What does this mean for you? If you’re shopping in cities like Dayton, Cincinnati, Columbus, or Springfield, these limits should cover the majority of available homes, especially since Ohio’s median home price is well below the FHA limit.

However, if you’re looking at more expensive properties—say, a $700,000 house in a high-end neighborhood—you might need to explore jumbo loan options or arrange extra money to cover the variance.

Benefits of Using an FHA Loan in Ohio

Accessible for First-Time Homebuyers

Let’s face it—saving for a 20% down payment can feel like climbing a financial mountain, especially if you’re juggling student loans, car payments, and everyday bills. FHA loans come to the rescue by requiring just 3.5% down, which can make a massive difference for first-time buyers.

For example, on a $215,000 home, you’d need $43,000 for a 20% down payment with a conventional loan. But with an FHA loan, that drops to just $7,525—a far more realistic number for most of us. FHA loan Ohio for first-time home buyers is one of the 8 Hacks To Buying Your First Home.

Lenient Credit Requirements

Did you know that Ohio’s average credit score is 716? You heard me right! That’s solid, but not everyone can hit that mark, and that is also a reality. FHA loans make homeownership possible for buyers with scores as low as 580 (or even 500 with a larger down payment). That’s a huge relief for anyone working to improve their credit while still wanting to buy a home.

Competitive Interest Rates

Who doesn't like low interest rates? Only Aliens from other planets can't have any problem with high interest rates. Haha. FHA loans in Ohio frequently have cheaper interest rates than other types of loans. Because they’re insured by the Government, lenders are willing to offer rates that, over the course of your loan, might save you hundreds of dollars.

Assistance With Closing Costs

You will see that closing costs in Ohio usually run between 2–5% of the home’s price, which can be a hefty expense. And here again, FHA loans allow sellers, lenders, or even gift funds to help cover these costs, meaning less financial stress for you when it’s time to sign on the dotted line.

Challenges and Drawbacks of FHA Loans

Mortgage Insurance Premiums (MIP)

Nothing is perfect, right? FHA loans also have some challenges and drawbacks. I am going to discuss it here so that you can get an idea of them and face and solve them firmly.

Insurance Premiums (MIP). When you take out an FHA loan, you’ll need to pay both:

- An upfront MIP (1.75% of the loan amount) at closing.

- Annual MIP payments are divided into monthly installments.

Let me give you an example. Let's say that you want a $200,000 FHA loan. Then, the upfront MIP would be $3,500 for you, and the annual premiums could add hundreds of dollars to your monthly payment. While this might feel like a burden, it’s the trade-off for getting a loan with such flexible requirements.

Primary Residence Requirement

You should keep in mind that FHA loans are only available for primary residences. If you want to buy a vacation home or an investment property, you can't use an FHA loan for this. If your plan is to purchase a rental property, you’ll need to explore conventional loans or other options.

Property Condition Standards

Since this loan is backed by the Government, they have some standards to follow, such as safety and livability standards. If you’re eyeing a fixer-upper that needs major repairs, you might need to use an FHA 203(k) loan. This FHA loan term can allow you to finance both the purchase and renovations. Otherwise, you’ll need to make repairs before the loan is approved.

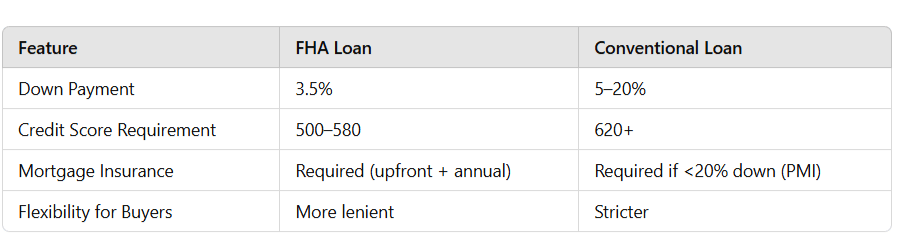

FHA Loan vs. Conventional Loan: Which is Better?

You can get a little idea of the difference between these two types of loans from this table below:

Which Loan Should You Choose?

Is your credit score below 620? Are you working with limited savings? If yes, then I would say that an FHA loan is likely to be your best option. However, if you’re in a strong financial position and can put down at least 20%, then you should go for a conventional loan, which might save you money in the long run since you can avoid private mortgage insurance (PMI).

Here Are Few Tips For First-Time Homebuyers in Ohio

You Should Create a Realistic Budget At First Place

You don’t want to end up house-poor, right? Start by crunching the numbers to see how much you can comfortably spend—not just on your mortgage but also on taxes, insurance, and maintenance. Experts recommend keeping housing costs below 30% of your monthly income.

Go For Pre-Approved Before Hunting A House

In chess, the minister is the most powerful. In card play, you keep a trump card, right? In the home buying process, pre-approval for an FHA loan could be your trump card. Not only does it show sellers that you’re serious, but it also helps you set a clear budget. Additionally, in competitive areas like Cincinnati, having a pre-approval letter provides you an advantage over other purchasers. Here in our blog, Getting Better Mortgage Pre-approval, you may find some useful tips.

Work With a Local Real Estate Agent

Let me tell you something before you skip this part. Agents are mostly paid by sellers, not by buyers. A knowledgeable agent is able to understand Ohio’s real estate market and can help you find properties that meet FHA requirements. Whether you’re buying in Dayton, Columbus, or Cincinnati, they will be able to guide you every step of the way. You can check this, which provides a full guide to choosing the right real estate agents in Cincinnati.

Cincinnati FHA Loan: What You Need to Know

If you’re looking to buy a home in Cincinnati, you’ve picked the right city. With a median home price of around $265,000, Cincinnati offers some of the best housing options in the country—especially compared to cities like Chicago or Columbus.

A 3.5% down payment is what you need to start, and a credit score as low as 580. With these, you could be on your way to owning a home in neighborhoods like Over-the-Rhine or Anderson Township. I know how overwhelming the process can feel, but trust me—FHA loans are built to make things easier for buyers like you. Let’s break it all down and explore how FHA loans fit perfectly into Cincinnati’s real estate market.

Why Choose an FHA Loan in Cincinnati?

What are you looking for? Affordable homes or historic neighborhoods and a thriving job market? You will find it all in Cincinnati. Over-the-Rhine’s charm, Mason’s family-friendly vibe, there’s a neighborhood for everyone.

You can see why FHA loans shine here:

- You can start with a low down payment. You can purchase a house with just a 3.5% down payment. No need for that hefty 20% most conventional loans require.

- You don't have to worry about your credit score. Got a 580 credit score? You’re eligible. Even if your credit isn’t perfect, an FHA loan has your back.

- You have affordable options. Cincinnati’s housing market is super accessible compared to other big cities, making it a great place to settle down.

The limits of FHA Loan in Cincinnati

Let's see some real numbers. For 2025, the FHA loan limit in Hamilton County is $472,030 for single-family homes. That covers most homes in the city, whether you’re eyeing a cozy spot in Price Hill or a sleek home in Hyde Park.

Looking at duplexes or multi-family homes? The limits are even higher, giving you room to invest—and maybe even rent out a unit to help pay your mortgage.

Working with Local Real Estate Agents

Navigating Cincinnati’s diverse neighborhoods can be tricky, but a local real estate agent makes it easier. They’ll help you find FHA-approved properties, guide you through areas like Over-the-Rhine or West Chester, and handle the nitty-gritty details. A good agent = less stress for you. Team leader of DreamX.Homes Ben Wourms is a top-rated agent in Cincinnati. You can reach him at this number: +1(513) 822-3764 or this email: ben@dreamxhomes.com if you have any questions.

FAQs

What credit score do I need to qualify for an FHA loan?

Most Ohio lenders require a minimum credit score of 580 for a 3.5% down payment. If your score is below 579 and above 500, you may still qualify by putting down 10%.

What is the income limit for FHA loans in Ohio?

No, FHA loans do not have strict income limits. However, your debt-to-income ratio (DTI) must meet FHA guidelines, which typically recommend keeping your DTI at or below 43%.

Can I refinance an FHA loan?

Yes, you can refinance an FHA loan using programs like FHA Streamline Refinancing. This option simplifies the process and often comes with lower fees and minimal paperwork for existing FHA borrowers.

Can I buy a fixer-upper with an FHA loan?

Absolutely! FHA offers a 203(k) loan, which allows you to finance the purchase of a home and the cost of renovations in one single mortgage. This is a great option if you’re looking to turn a fixer-upper into your dream home.

Do FHA loans have lower interest rates?

Yes, FHA loans often come with competitive interest rates because they’re insured by the Federal Government. However, your rate will also be determined by your credit score you have and the lender you choose.

Summary

I hope that you got all your answers. If you’re looking for affordability and flexibility, then you should go for buying a house with an FHA loan Ohio. This could be one of the smartest moves in your home-buying journey. With low down payments, lenient credit requirements, and plenty of assistance programs, FHA loans open doors for countless Ohioans every year.

If you are aiming for a home in Cincinnati, charming Dayton, or anywhere in between, FHA loans can make this happen. So, why wait? Start exploring your options today—you’re closer than you think to unlocking the door to your future.

Categories

- All Blogs 92

- Boosting Home Value 3

- Buyer Resources 13

- Eco-Friendly Upgrades 1

- First-Time Buyer Tips 2

- Home Buying & Selling 3

- Home Improvement & Staging 5

- Investment & Financing 14

- Local Attractions & Schools 5

- Local Market Trends 8

- Local Policy Changes 2

- Market & Industry News 2

- Market Insights 6

- Mistakes to Avoid 1

- Mortgage & Financing 22

- Neighborhood Spotlights 12

- Neighborhoods & Lifestyle 18

- New Construction 10

- Real Estate News & Updates 4

- Real Estate Technology 2

- Seller Resources 4

- Staging Tips 2

- Sustainability 3

Recent Posts

Tired of Feeling Lost in the Home Loan Maze?

Get 5 Insider Secrets from NAR(National Association of Realtors) that Make Navigating Your Loan Simple and Stress-Free!

I consent to receive calls and texts from DreamX Homes & Glasshouse Realty Group for real estate information and assistance. You can unsubscribe anytime.

"My job is to find and attract mastery-based agents to the office, protect the culture, and make sure everyone is happy! "